The new tax incentive for scientific research and innovation offers businesses significant benefits, serving as a modern alternative to the Non-Habitual Resident (NHR) scheme.

Designed to encourage investment in cutting-edge projects, this incentive provides financial advantages for companies.

In this article, we will explore how this new tax incentive works, its key advantages, and practical steps companies can take to benefit from it.

What is NHR?

The NHR regime, introduced by the Portuguese Personal Income Tax Code through Decree-Law no. 249/2009 and completed by Decree no. 12/2010, aimed to attract highly skilled professionals, high net-worth individuals, and foreign pensioners to Portugal.

It has been a competitive scheme since its inception. However, in October 2023, the Portuguese Government announced the end of the NHR regime. This was confirmed on December 29, 2023, when the State Budget Law for 2024 revoked the NHR regime effective January 1, 2024.

The new State Budget Law has introduced a replacement regime to attract highly skilled professionals in specific areas, with different rules and tax benefits from the NHR.

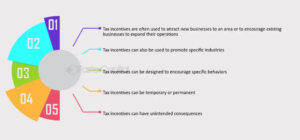

Key Features of the New Tax Incentive: Source: Fastercapital.com

- Encourages Investment: Stimulates investment in research and development activities.

- Support for Growth: Supports the growth and expansion of businesses in Portugal.

- Qualifying Expenses: Covers costs like staffing, equipment, and operational expenses.

- Financial Relief: Aims to ease the financial burden on businesses and researchers for ambitious projects.

Comparing the New Incentive with the NHR Scheme

While the NHR scheme was successful in attracting foreign talent, the new tax incentive is more inclusive. It targets a broader audience, including both local and international researchers, regardless of their residency status. This inclusive approach aims to foster a more diverse and dynamic research environment.

THE SCIENTIFIC RESEARCH AND INNOVATION REGIME

The new tax incentive program in Portugal aims to benefit individuals in various fields like teaching, research, and qualified jobs. It offers a 20% flat tax rate for 10 years to those involved in specific activities, encouraging their continued engagement.

This program covers a wide range of professions, including teaching in higher education, scientific research, jobs related to productive investment, and activities in specific regions like Madeira and Azores. It also extends to jobs in certified startups, entities contributing to the national economy, and highly skilled professions.

Under this regime, net income from employment and self-employment is taxed at a flat rate, providing financial stability to participants. However, pension income falls under general progressive rates, potentially reaching a 53% nominal tax rate.

The program’s benefits are contingent upon tax residency and ongoing engagement in eligible activities each year. It requires registration and has specific tax rules for income from non-resident entities in blacklisted jurisdictions.

Exceptions apply to individuals who previously benefited from similar tax schemes, and each taxpayer can utilize this program only once.

Case Studies

Ireland’s Research and Development Tax Credit: Ireland introduced a Research and Development (R&D) Tax Credit in 2004, offering a 25% tax credit for eligible R&D expenditures. This incentive led to a surge in R&D investments, with companies like Google, Intel, and Pfizer expanding their R&D activities in Ireland. The tax credit encouraged innovation and contributed to Ireland’s reputation as a hub for technology and pharmaceutical research.

Singapore’s Productivity and Innovation Credit (PIC) Scheme: Singapore implemented the PIC Scheme in 2010, providing tax deductions and cash payouts for businesses investing in innovation and productivity improvements. The scheme resulted in a 23% increase in R&D spending among local enterprises and attracted multinational corporations to establish R&D centers in Singapore. The PIC Scheme boosted Singapore’s competitiveness and drove economic growth through innovation-led initiatives.

Application Process

If you’re interested in applying for this tax incentive, here’s a quick guide to get you started:

- Identify Eligible Projects: Ensure your research or innovation project meets the criteria.

- Prepare Documentation: Gather all necessary documents, including project proposals, budgets, and proof of expenses.

- Submit Application: Follow the official submission process, which may include online forms and physical documentation.

- Await Approval: The approval process may take some time, so be prepared for a waiting period.

- Utilize Funds: Once approved, you can start utilizing the tax benefits to support your project.

Future Prospects

Looking ahead, there’s a strong potential for this tax incentive to expand and evolve. As more businesses and researchers take advantage of the benefits, the government may introduce additional improvements and support mechanisms. The future looks promising for scientific research and innovation.

Frequently Asked Questions (FAQs)

Q: What is the main difference between the new tax incentive and the NHR scheme?

The new tax incentive focuses on supporting scientific research and innovation, while the NHR scheme was aimed at attracting foreign professionals through tax benefits.

Q: Who is eligible for the new tax incentive?

Both businesses and individual researchers conducting qualifying R&D activities are eligible.

Q: What types of expenses qualify for the tax incentive?

Qualifying expenses can include staffing costs, equipment purchases, and certain operational expenses related to R&D.

Q: How do I apply for the new tax incentive?

The application involves submitting detailed project proposals and documentation to demonstrate eligibility.

Q: What are the benefits of this tax incentive for researchers?

Researchers can receive financial support for their projects, helping to fund innovative studies and advance their careers.

Final Thoughts

The new tax incentive for scientific research and innovation offers an exciting alternative to the NHR scheme. By providing substantial tax benefits, it aims to reduce financial barriers and stimulate investment in R&D activities.

Whether you’re a business looking to innovate or a researcher with groundbreaking ideas, this incentive presents a valuable opportunity to advance your projects and contribute to scientific progress. So, Start exploring how you can benefit from this initiative today!

Getmenif.com helps you get your Portuguese NIF quickly and easily. Just fill out the form, upload documents, and make the payment – and you’re done!